Estimating the inflation equation (Page 325)

library("foreign")

data = read.dta("Dataset/macro.dta")

data = na.omit(data)

library("systemfit")

eq1 = data$inflation ~ data$dprod + data$dcredit + data$dmoney + data$rsandp

eq2 = data$rsandp ~ data$dprod + data$dspread + data$rterm + data$inflation

inst = ~ income + farmPrice + trend

eqSystem = list(eq1, eq2)

SEM = systemfit(eqSystem,method="SUR")

SEM$eq[[1]]$coefficients

## (Intercept) data$dprod data$dcredit data$dmoney data$rsandp

## 2.505916e-01 -1.258143e-02 1.512073e-06 -4.161894e-03 1.702656e-04

## (Intercept) data$dprod data$dspread data$rterm data$inflation

## 0.8417346 -0.2741500 -8.4161465 -0.3354731 -0.9654215

library(foreign)

library(systemfit)

data <- na.omit(read.dta("Dataset/macro.dta"))

eqSystem <- list(

inflation ~ dprod + dcredit + dmoney + rsandp,

rsandp ~ dprod + dspread + rterm + inflation

)

inst <- ~ income + farmPrice + trend

SEM <- systemfit(eqSystem, method = "SUR", inst = inst, data = data)

#SUR estimates for 'eq1' (equation 1)

SEM$eq[[1]]$coefficients

## (Intercept) dprod dcredit dmoney rsandp

## 2.505916e-01 -1.258143e-02 1.512073e-06 -4.161894e-03 1.702656e-04

# SUR estimates for 'eq2' (equation 2)

SEM$eq[[2]]$coefficients

## (Intercept) dprod dspread rterm inflation

## 0.8417346 -0.2741500 -8.4161465 -0.3354731 -0.9654215

VAR estimation (Page 345)

data = read.dta("Dataset/currencies.dta")

data = na.omit(data)

library("vars")

Y = data.frame(reur=data$reur,rgbp=data$rgbp,rjpy=data$rjpy)

VAR.cur = VAR(Y,p=2)

summary(VAR.cur)

##

## VAR Estimation Results:

## =========================

## Endogenous variables: reur, rgbp, rjpy

## Deterministic variables: const

## Sample size: 3985

## Log Likelihood: -6043.54

## Roots of the characteristic polynomial:

## 0.3329 0.3329 0.1532 0.1146 0.1146 0.002806

## Call:

## VAR(y = Y, p = 2)

##

##

## Estimation results for equation reur:

## =====================================

## reur = reur.l1 + rgbp.l1 + rjpy.l1 + reur.l2 + rgbp.l2 + rjpy.l2 + const

##

## Estimate Std. Error t value Pr(>|t|)

## reur.l1 0.200155 0.022708 8.814 <2e-16 ***

## rgbp.l1 -0.061566 0.024107 -2.554 0.0107 *

## rjpy.l1 -0.020151 0.016658 -1.210 0.2265

## reur.l2 -0.033413 0.022619 -1.477 0.1397

## rgbp.l2 0.024656 0.024079 1.024 0.3059

## rjpy.l2 0.002628 0.016682 0.158 0.8748

## const -0.005836 0.007453 -0.783 0.4337

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

##

## Residual standard error: 0.4703 on 3978 degrees of freedom

## Multiple R-Squared: 0.02548, Adjusted R-squared: 0.02401

## F-statistic: 17.33 on 6 and 3978 DF, p-value: < 2.2e-16

##

##

## Estimation results for equation rgbp:

## =====================================

## rgbp = reur.l1 + rgbp.l1 + rjpy.l1 + reur.l2 + rgbp.l2 + rjpy.l2 + const

##

## Estimate Std. Error t value Pr(>|t|)

## reur.l1 -4.278e-02 2.079e-02 -2.058 0.039687 *

## rgbp.l1 2.616e-01 2.207e-02 11.855 < 2e-16 ***

## rjpy.l1 -5.664e-02 1.525e-02 -3.714 0.000207 ***

## reur.l2 5.677e-02 2.071e-02 2.741 0.006144 **

## rgbp.l2 -9.210e-02 2.204e-02 -4.178 3.01e-05 ***

## rjpy.l2 2.964e-03 1.527e-02 0.194 0.846115

## const 4.539e-05 6.823e-03 0.007 0.994693

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

##

## Residual standard error: 0.4306 on 3978 degrees of freedom

## Multiple R-Squared: 0.05224, Adjusted R-squared: 0.05081

## F-statistic: 36.55 on 6 and 3978 DF, p-value: < 2.2e-16

##

##

## Estimation results for equation rjpy:

## =====================================

## rjpy = reur.l1 + rgbp.l1 + rjpy.l1 + reur.l2 + rgbp.l2 + rjpy.l2 + const

##

## Estimate Std. Error t value Pr(>|t|)

## reur.l1 0.0241862 0.0225072 1.075 0.28262

## rgbp.l1 -0.0679786 0.0238946 -2.845 0.00446 **

## rjpy.l1 0.1508446 0.0165107 9.136 < 2e-16 ***

## reur.l2 -0.0313338 0.0224194 -1.398 0.16231

## rgbp.l2 0.0324034 0.0238668 1.358 0.17464

## rjpy.l2 0.0007184 0.0165350 0.043 0.96535

## const -0.0036822 0.0073871 -0.498 0.61818

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

##

## Residual standard error: 0.4662 on 3978 degrees of freedom

## Multiple R-Squared: 0.0243, Adjusted R-squared: 0.02283

## F-statistic: 16.51 on 6 and 3978 DF, p-value: < 2.2e-16

##

##

##

## Covariance matrix of residuals:

## reur rgbp rjpy

## reur 0.22118 0.1417 0.06108

## rgbp 0.14168 0.1854 0.03390

## rjpy 0.06108 0.0339 0.21730

##

## Correlation matrix of residuals:

## reur rgbp rjpy

## reur 1.0000 0.6997 0.2786

## rgbp 0.6997 1.0000 0.1689

## rjpy 0.2786 0.1689 1.0000

VAR Lag Order Selection Criteria (Page 347)

## $selection

## AIC(n) HQ(n) SC(n) FPE(n)

## 2 2 1 2

##

## $criteria

## 1 2 3 4 5 6 7

## AIC(n) -5.459940719 -5.468184042 -5.46562649 -5.465133664 -5.464543930 -5.463005327 -5.463004834

## HQ(n) -5.453212977 -5.456410494 -5.44880713 -5.443268504 -5.437632964 -5.431048554 -5.426002255

## SC(n) -5.440966769 -5.434979631 -5.41819162 -5.403468328 -5.388648133 -5.372879067 -5.358648113

## FPE(n) 0.004253808 0.004218887 0.00422969 0.004231776 0.004234272 0.004240793 0.004240795

## 8 9 10

## AIC(n) -5.462101652 -5.460006431 -5.457433090

## HQ(n) -5.420053268 -5.412912240 -5.405293093

## SC(n) -5.343514469 -5.327188785 -5.310384982

## FPE(n) 0.004244628 0.004253531 0.004264492

VAR Granger Causality (Page 348)

grangertest(reur~rgbp,order=1,data=Y)

## Granger causality test

##

## Model 1: reur ~ Lags(reur, 1:1) + Lags(rgbp, 1:1)

## Model 2: reur ~ Lags(reur, 1:1)

## Res.Df Df F Pr(>F)

## 1 3983

## 2 3984 -1 5.4299 0.01984 *

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

grangertest(reur~rjpy,order=1,data=Y)

## Granger causality test

##

## Model 1: reur ~ Lags(reur, 1:1) + Lags(rjpy, 1:1)

## Model 2: reur ~ Lags(reur, 1:1)

## Res.Df Df F Pr(>F)

## 1 3983

## 2 3984 -1 1.1067 0.2929

grangertest(rgbp~reur,order=1,data=Y)

## Granger causality test

##

## Model 1: rgbp ~ Lags(rgbp, 1:1) + Lags(reur, 1:1)

## Model 2: rgbp ~ Lags(rgbp, 1:1)

## Res.Df Df F Pr(>F)

## 1 3983

## 2 3984 -1 4.6618 0.0309 *

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

grangertest(rgbp~rjpy,order=1,data=Y)

## Granger causality test

##

## Model 1: rgbp ~ Lags(rgbp, 1:1) + Lags(rjpy, 1:1)

## Model 2: rgbp ~ Lags(rgbp, 1:1)

## Res.Df Df F Pr(>F)

## 1 3983

## 2 3984 -1 16.108 6.093e-05 ***

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

grangertest(rjpy~reur,order=1,data=Y)

## Granger causality test

##

## Model 1: rjpy ~ Lags(rjpy, 1:1) + Lags(reur, 1:1)

## Model 2: rjpy ~ Lags(rjpy, 1:1)

## Res.Df Df F Pr(>F)

## 1 3983

## 2 3984 -1 1.8463 0.1743

grangertest(rjpy~rgbp,order=1,data=Y)

## Granger causality test

##

## Model 1: rjpy ~ Lags(rjpy, 1:1) + Lags(rgbp, 1:1)

## Model 2: rjpy ~ Lags(rjpy, 1:1)

## Res.Df Df F Pr(>F)

## 1 3983

## 2 3984 -1 7.984 0.004743 **

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

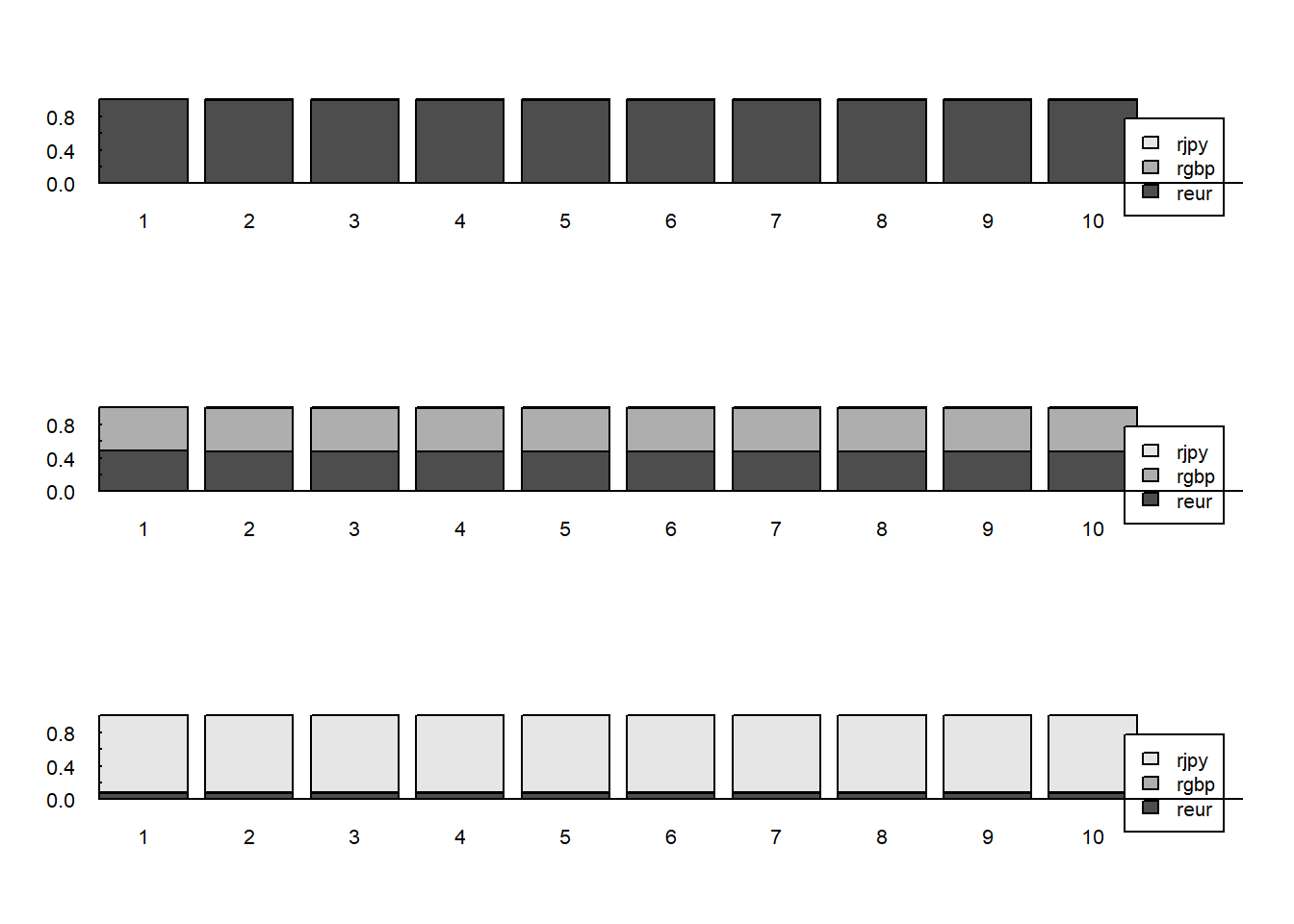

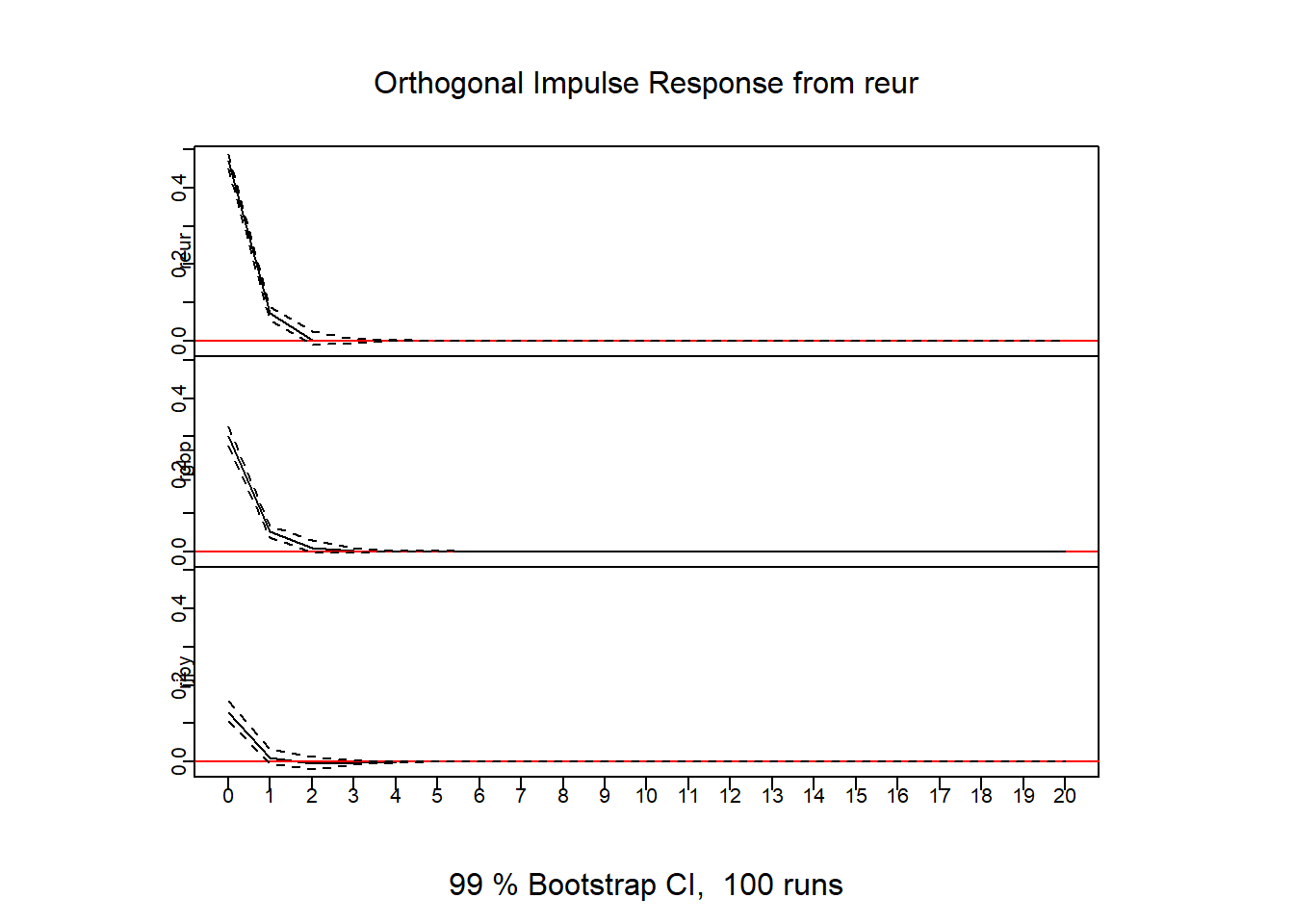

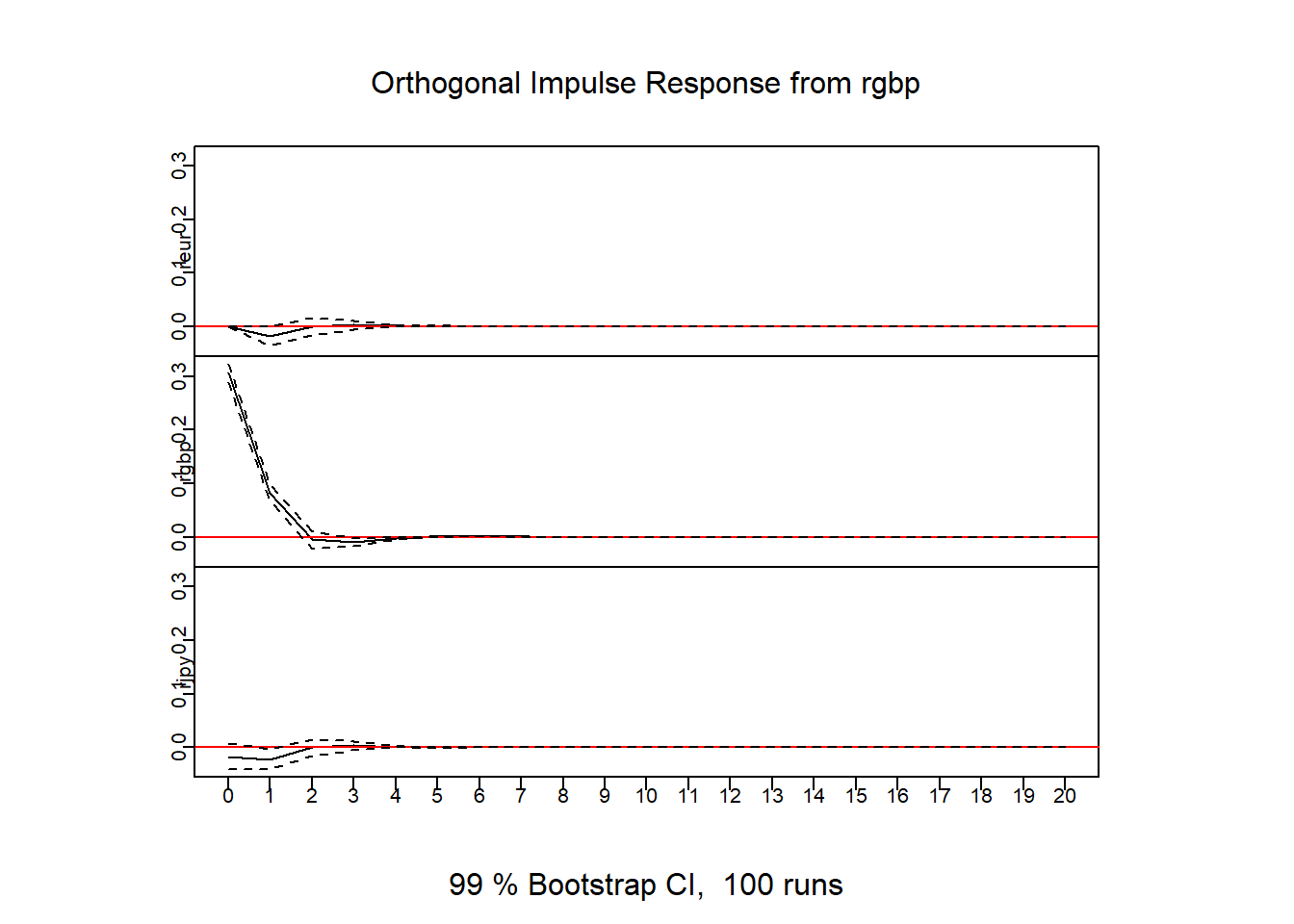

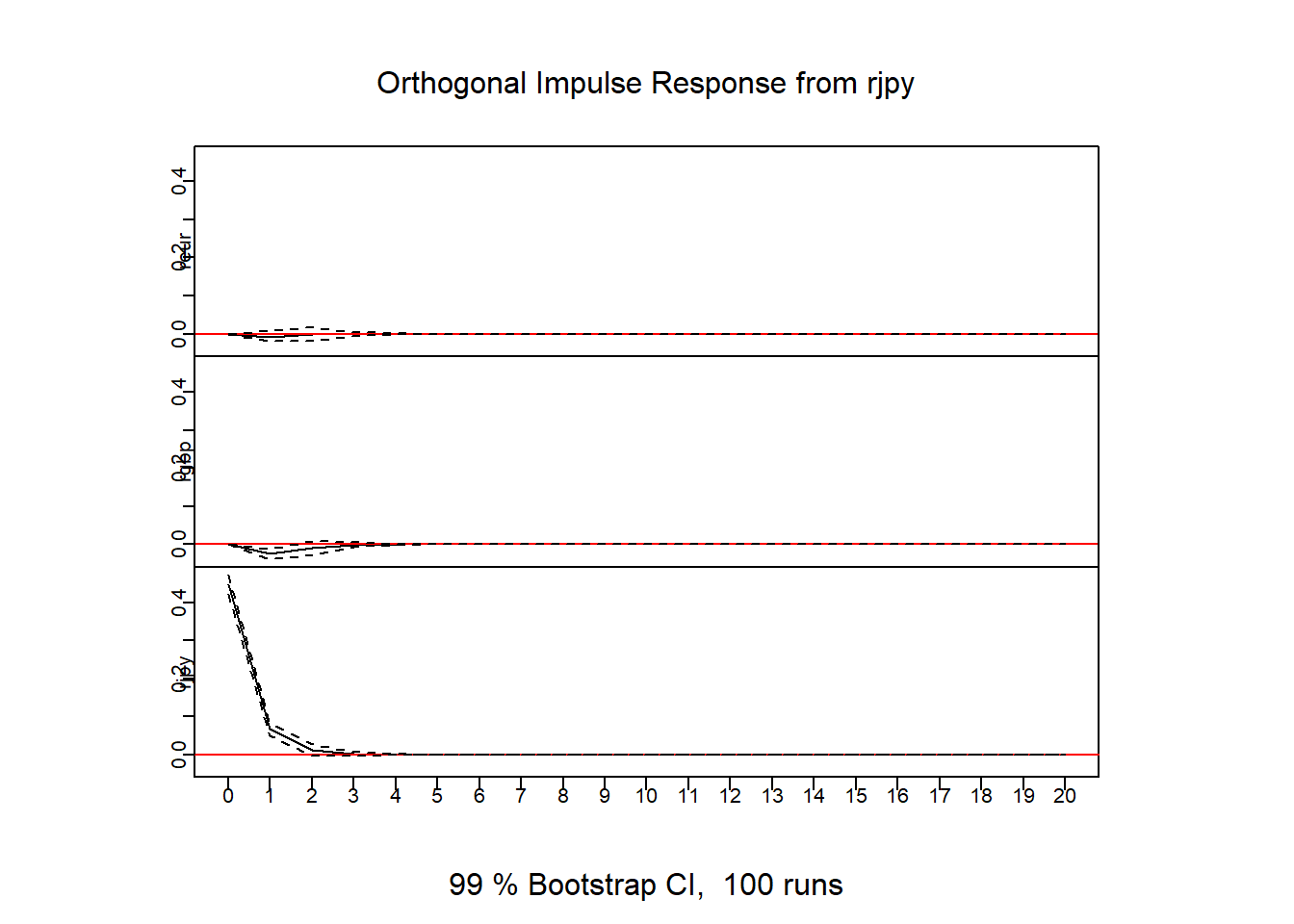

Screenshot 7.5 Combined impulse response graphs (Page 349)

par(mfcol = c(3,1), oma = c(0,0,1,0) + 0.2, mar = c(0,1,0,0) + 1, mgp = c(0, 0.2, 0))

irf.cur = irf(VAR.cur,n.ahead=20,ortho=TRUE,boot=TRUE,ci=0.99)

plot(irf.cur,col=1)

Screenshot 7.6 Variance decomposition graphs (Page 350)

fevd.cur <- fevd(VAR.cur)

fevd.cur

## $reur

## reur rgbp rjpy

## [1,] 1.0000000 0.000000000 0.0000000000

## [2,] 0.9981178 0.001524051 0.0003581120

## [3,] 0.9981148 0.001526281 0.0003589032

## [4,] 0.9980823 0.001558801 0.0003589082

## [5,] 0.9980779 0.001563074 0.0003589907

## [6,] 0.9980779 0.001563074 0.0003590174

## [7,] 0.9980779 0.001563127 0.0003590180

## [8,] 0.9980778 0.001563133 0.0003590181

## [9,] 0.9980778 0.001563133 0.0003590181

## [10,] 0.9980778 0.001563133 0.0003590181

##

## $rgbp

## reur rgbp rjpy

## [1,] 0.4895160 0.5104840 0.000000000

## [2,] 0.4781687 0.5185439 0.003287417

## [3,] 0.4781410 0.5181839 0.003675103

## [4,] 0.4779089 0.5184136 0.003677557

## [5,] 0.4778931 0.5184284 0.003678533

## [6,] 0.4778929 0.5184284 0.003678769

## [7,] 0.4778925 0.5184287 0.003678767

## [8,] 0.4778925 0.5184287 0.003678769

## [9,] 0.4778925 0.5184287 0.003678769

## [10,] 0.4778925 0.5184287 0.003678769

##

## $rjpy

## reur rgbp rjpy

## [1,] 0.07763026 0.001327719 0.9210420

## [2,] 0.07630518 0.003773124 0.9199217

## [3,] 0.07636047 0.003771074 0.9198685

## [4,] 0.07636993 0.003828557 0.9198015

## [5,] 0.07636975 0.003834408 0.9197958

## [6,] 0.07636976 0.003834414 0.9197958

## [7,] 0.07636976 0.003834499 0.9197957

## [8,] 0.07636976 0.003834506 0.9197957

## [9,] 0.07636976 0.003834506 0.9197957

## [10,] 0.07636976 0.003834506 0.9197957

plot(fevd.cur,las=1,xlab="",ylab="",main="",xaxs="i",yaxs="i",tck=.02)