Screenshot 3.2. Summary statistics for spot and futures (Page 88)

library(foreign)

library(moments)

data_sp <- read.dta("Dataset/SandPhedge.dta")

data_sp$Date <- seq(2002 + 2/12, 2013 + 4/12, by = 1/12)

data_sp <- na.omit(data_sp)

Y <- cbind(rspot = data_sp$rspot, rfutures = data_sp$rfutures)

summary_stats <- data.frame(

Mean = apply(Y, 2, mean),

Median = apply(Y, 2, median),

Max = apply(Y, 2, max),

Min = apply(Y, 2, min),

SD = apply(Y, 2, sd),

Skewness = apply(Y, 2, skewness),

Kurtosis = apply(Y, 2, kurtosis)

)

jarque_tests <- lapply(1:2, function(i) jarque.test(Y[, i]))

names(jarque_tests) <- colnames(Y)

summary_stats

## Mean Median Max Min SD Skewness Kurtosis

## rspot 0.2739265 1.101731 10.06554 -18.38397 4.591529 -0.9111043 4.740732

## rfutures 0.2713085 1.024841 10.39119 -18.80256 4.548128 -0.9275250 4.878594

## $rspot

##

## Jarque-Bera Normality Test

##

## data: Y[, i]

## JB = 35.457, p-value = 1.998e-08

## alternative hypothesis: greater

##

##

## $rfutures

##

## Jarque-Bera Normality Test

##

## data: Y[, i]

## JB = 38.918, p-value = 3.541e-09

## alternative hypothesis: greater

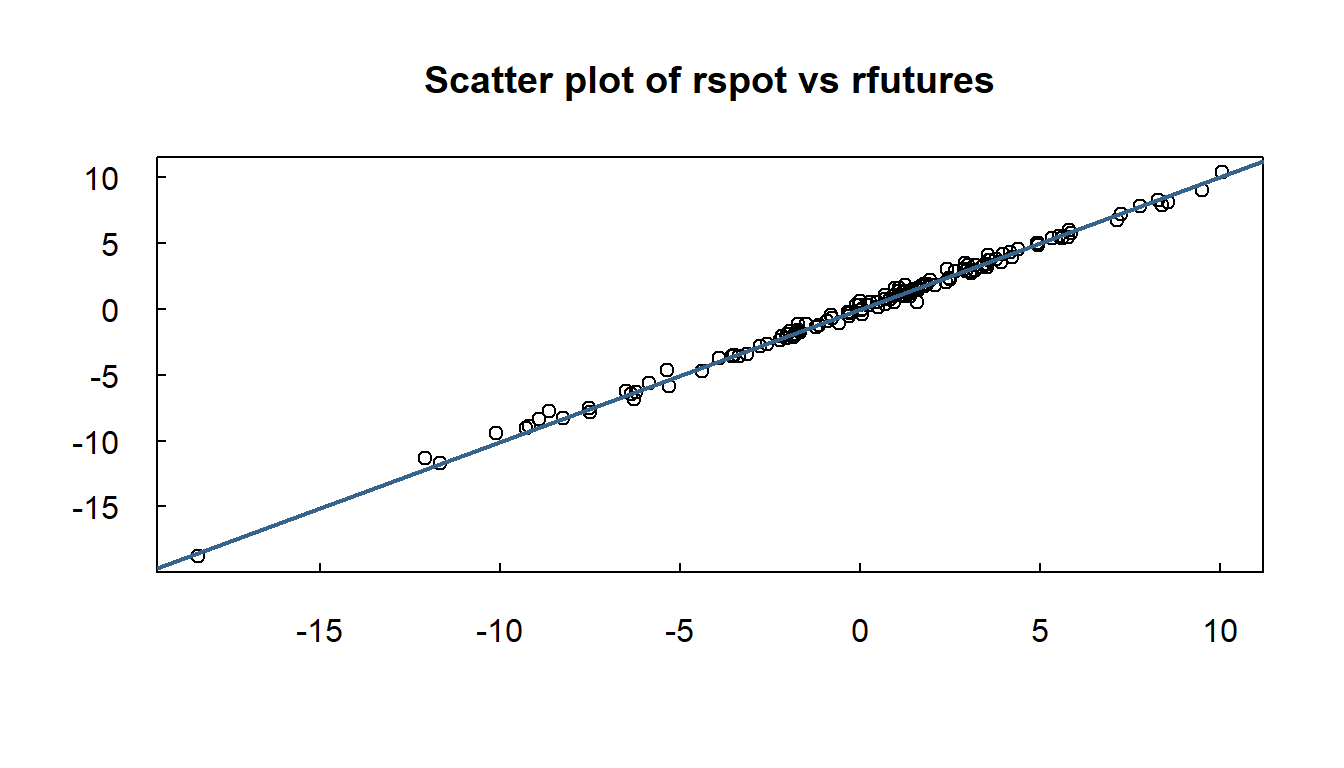

Screenshot 3.4 Regression Estimation results (Page 90)

plot(Y, type = "p", las = 1, xlab = "", ylab = "", main = "Scatter plot of rspot vs rfutures", tck = 0.02)

lm_sp <- lm(rspot ~ rfutures, data = data_sp)

abline(lm_sp, col = "steelblue4", lwd = 2)

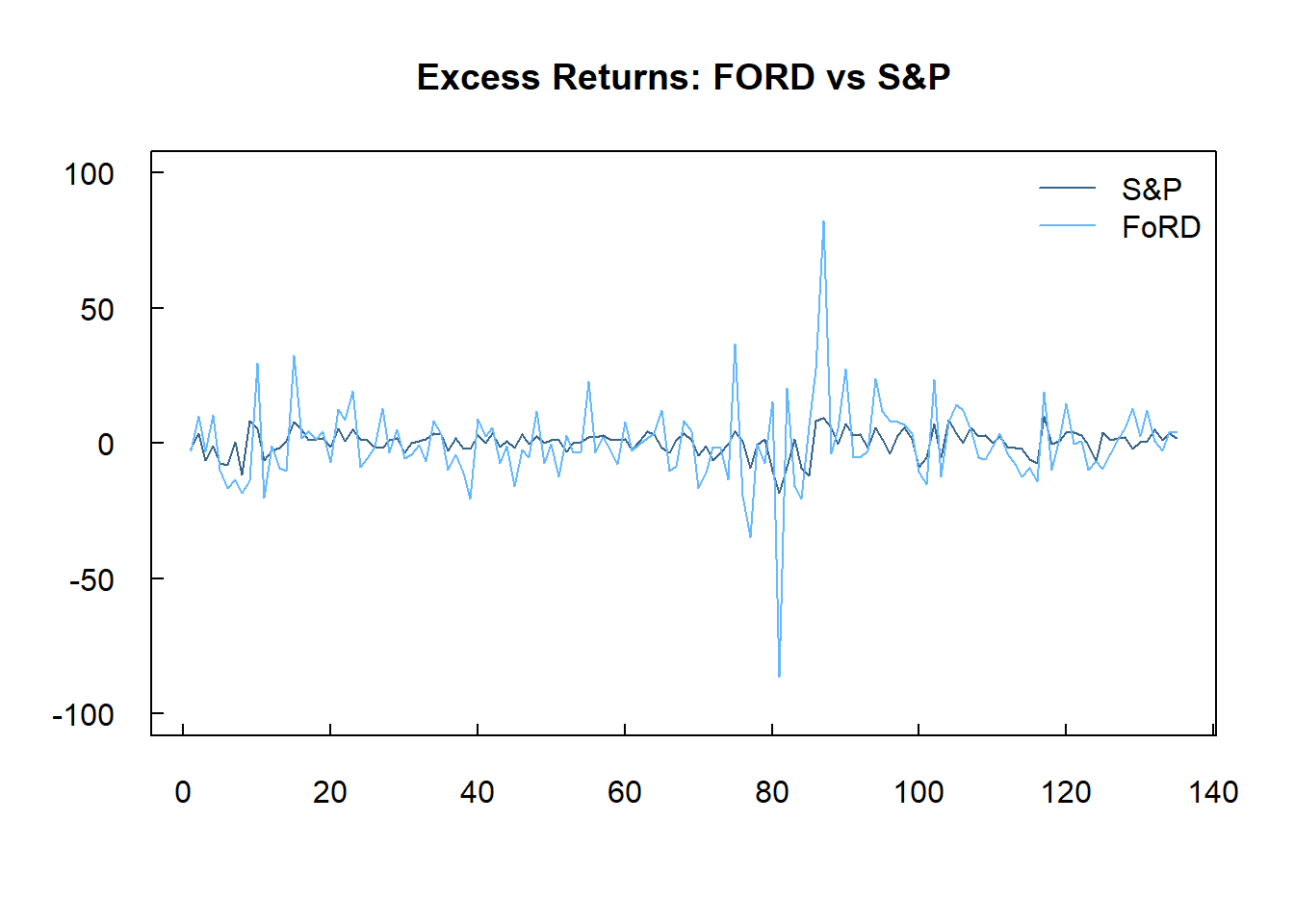

CAPM Data Prep (Page 123)

data_capm <- read.dta("Dataset/capm.dta")

data_capm$Date <- seq(2002 + 1/12, 2013 + 4/12, by = 1/12)

rsandp <- 100 * diff(log(data_capm$SANDP))

rford <- 100 * diff(log(data_capm$FORD))

ustb3m <- data_capm$USTB3M[-1] / 12

# Excess returns

erford <- rford - ustb3m

ersandp <- rsandp - ustb3m

Screenshot 3.5 Plot of the two series (PP 125)

# Plot the first series

plot(ersandp, type = "l", las = 1, col = "steelblue4",

main = "Excess Returns: FORD vs S&P", xlab = "", ylab = "", ylim = c(-100, 100), tck = 0.02)

# Add the second series

lines(erford, type = "l", col = "steelblue1")

legend("topright", legend = c("S&P", "FoRD"),

col = c("steelblue4", "steelblue1"), lty = 1, bty = "n")

CAPM Regression Table (Page 126)

summary(lm_capm <- lm(erford ~ ersandp))

##

## Call:

## lm(formula = erford ~ ersandp)

##

## Residuals:

## Min 1Q Median 3Q Max

## -48.797 -7.294 -1.225 5.593 63.461

##

## Coefficients:

## Estimate Std. Error t value Pr(>|t|)

## (Intercept) -0.4475 1.0886 -0.411 0.682

## ersandp 2.0208 0.2383 8.481 3.76e-14 ***

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

## Residual standard error: 12.63 on 133 degrees of freedom

## Multiple R-squared: 0.351, Adjusted R-squared: 0.3461

## F-statistic: 71.93 on 1 and 133 DF, p-value: 3.758e-14